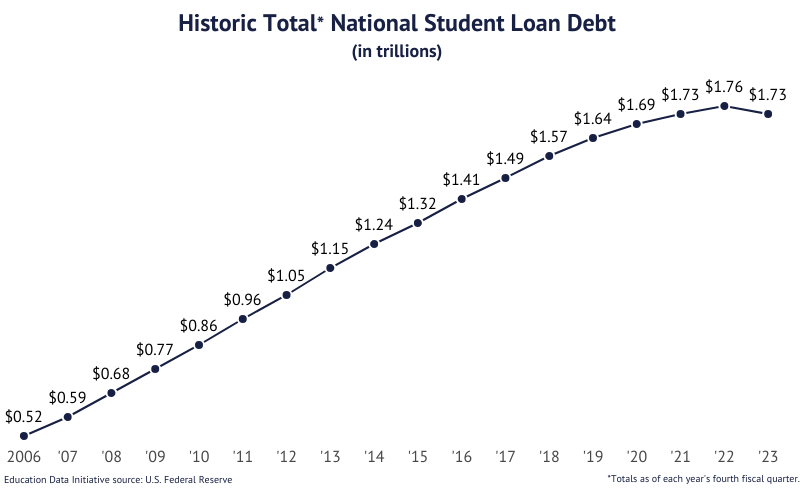

There is no denying that college tuition has reached insurmountable levels. Since 1980, tuition has increased by over 180%, with the average cost of higher education now exceeding $32,000 per year. As tuition costs rose, so too did the student debt burden—a burden that has now reached $1.75 trillion. Over the past few decades, different presidential administrations have approached this pressing issue in various ways. Over the last two years, President Joe Biden has chosen to combat the student debt crisis through direct measures—measures that involved canceling billions of dollars in student debt. As Biden’s presidency comes to an end, it’s essential to examine his approach to the problem and consider the potential long-term economic repercussions of his solutions.

Student loan relief programs and federal financial aid have a long history, with initiatives like the Higher Education Act of 1965 and the Basic Educational Opportunity Grant of 1972 highlighting the ongoing financial challenges of affording college and the relief measures established since the 20th century. Despite various relief programs, student debt has continued to rise. President Biden has always been a staunch advocate for student loan forgiveness programs and has, before his presidency, discussed plans to reduce the financial burden placed on students.

On August 24, 2022, President Biden introduced a comprehensive three-part student loan forgiveness plan to eliminate $430 billion in student debt. The first part offers $20,000 in debt cancellation for Pell Grant recipients and $10,000 for non-Pell Grant borrowers. The second part caps monthly payments on undergraduate loans at 5% of a borrower’s income and includes significant enhancements to the Public Service Loan Forgiveness (PSLF) program to simplify qualification. The third part promises to increase Pell Grant funding, make community college tuition-free and take measures to prevent future college tuition increases. With the average student loan debt at $38,000, this plan would have provided substantial relief, particularly for low-income and minority borrowers. It’s important to note that this forgiveness applies only to federal student loans, which constitute 90% of student debt, excluding loans from private lenders.

The program launched on October 14, 2022, but was temporarily suspended in November due to several lawsuits. Among these, a coalition of six Republican states argued that the program jeopardized their loan servicing revenues. The Supreme Court agreed to review the case and invalidated Biden’s three-part plan in a 6-3 ruling on June 30, 2023.

Yet, as of today, the Biden administration has forgiven $169 billion in student loans for 4.76 million borrowers through various existing relief programs. One major initiative is the Income-Driven Repayment (IDR) forgiveness program, which adjusts monthly payments based on income and family size and can forgive the remaining balance after 20-25 years of qualifying payments. Among the IDR plans, the Saving on Valuable Education (SAVE) program, introduced by Biden, is the most affordable and popular. In addition to the IDR plans, the Public Service Loan Forgiveness (PSLF) program targets government and non-profit employees, offering loan forgiveness after ten years of qualifying payments. Other loan relief options are available, including School-related Discharge Options, Teacher Loan Forgiveness, and Total and Permanent Disability Discharge.

After his three-part plan was dismissed, Biden introduced a “Plan B” for loan forgiveness. He announced that the Department of Education could implement debt relief through rulemaking under the Higher Education Act. By February 2024, a consensus emerged around Biden’s “Plan B” program, which could assist 30 million student borrowers in repaying their debt if it can successfully navigate legal challenges.

But what are the economic consequences of canceling student debt? Well, it’s important to understand that canceling student debt does not make the debt disappear. Instead, it’s added to the federal deficit. On the positive side, canceling student debt relieves borrowers of a significant financial burden, putting thousands of dollars in their pockets, and, eventually, back into the economy. Theoretically, think of it as an understated stimulus package. With a greater financial base, students will have an easier time starting businesses, buying homes, and being effective consumers—activities that will undoubtedly increase economic productivity. Additionally, student loan relief often targets low-income individuals, aiding those from disadvantaged backgrounds in building wealth.

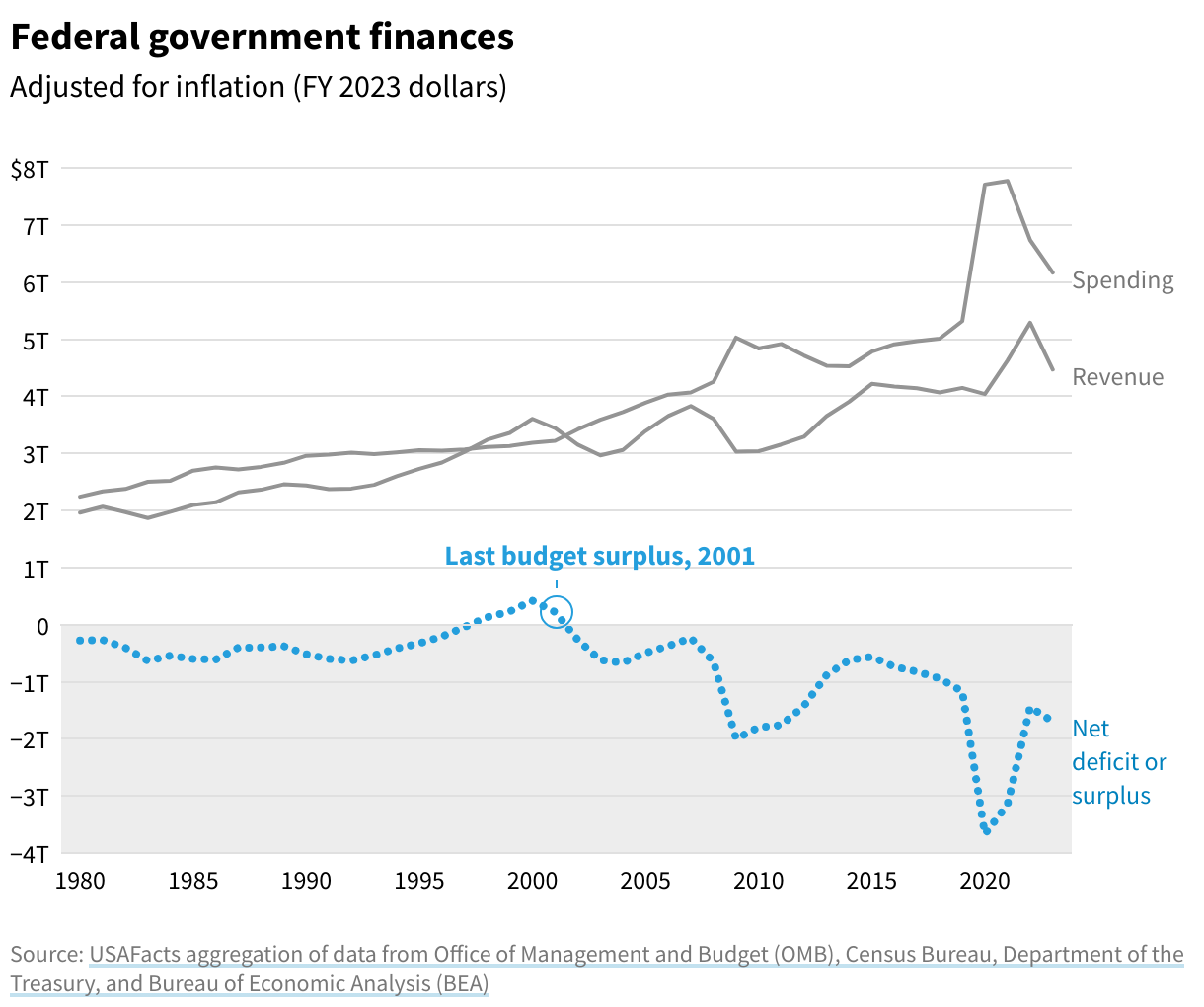

One downside of canceling debt is that the government’s increased spending could lead to inflationary pressures. However, estimates from various organizations suggest that any resulting inflation would likely be minimal. The primary concern with canceling student loans is its impact on the national debt, which is approaching $35 trillion. The federal deficit—the gap between federal spending and revenues—currently stands at $1.27 trillion and is only projected to rise. A growing federal deficit is unsustainable in the long term and could have severe economic consequences.

Rising federal debt means the government will need to allocate more funds to cover interest payments, reducing the amount available for public investment. Additionally, increased debt drives up the demand for money, leading to higher national interest rates. These higher rates can slow economic growth, depress wages for American workers, stifle innovation, and hinder the productivity of U.S. businesses. Moreover, in free market thinking investing in government bonds diverts funds away from private investment, which can further impact the future success of American corporations. A growing national debt also undermines public confidence in economic stability, exerting upward pressure on prices. Simply put, a high national debt adversely affects all aspects of our economy.

While President Biden’s current efforts to reduce student debt have not significantly impacted the federal deficit, ongoing debt cancellations could have that effect. Additionally, if students frequently depend on government debt relief, colleges might be incentivized to raise tuition even further. However, the rising federal deficit is not solely due to student debt cancellation; it is also a result of increased federal spending across the board. During Biden’s presidency, the national debt has risen by more than $6 trillion, with projections indicating a $7.9 trillion increase over his four-year term. Former President Donald Trump added $7.7 trillion to the national debt, reflecting a similarly substantial increase.

However, Biden’s increase in debt occurred during an inflationary period, where additional public spending could further drive up prices. In contrast, Trump’s debt increase happened during the COVID-19 pandemic, when heightened public spending was critically needed. Either way, attributing the national debt crisis to just two individuals oversimplifies the issue. The growth of the national debt over recent decades results from various presidential administrations’ policies, which have led to GDP growth struggling to keep pace with rising debt and spending. It is hoped that future administrations will implement measures to enhance economic growth and address the national debt more effectively.

Returning to the issue of student loans, Biden’s actions fall short of addressing the fundamental problem behind the significant borrower burden: exorbitant tuition costs. Instead, his programs merely provide temporary relief from the symptoms without tackling the underlying issue. Increasing college tuition lacks a simple solution. The government might consider boosting college funding, imposing a cap on tuition fees, or closely regulating college expenditures. However, each of these potential solutions comes with its own set of challenges.

Biden’s student debt relief programs also have significant ethical concerns. Funding these programs requires the government to cut spending—likely from essential social services—or raise taxes. The ethical dilemma with raising taxes is that it means American taxpayers are essentially covering the cost of college for others. The debt burden shifts from the student who took out loans and benefited from their education to the taxpayers, two-thirds of whom did not attend college. J.D. Vance, Trump’s future vice president, argued, “If you want to provide student debt relief, you should penalize those who have gained from this corrupt system, not ask plumbers in Ohio to subsidize the choices of college-educated individuals, many of whom will earn substantial incomes over their lifetimes.” On the other hand, Vice President Kamala Harris opts to follow Biden’s lead, stating “most people should not have to carry this kind of worry.”

Addressing the student debt crisis requires more than just temporary relief—it calls for systemic change. Although Biden’s debt cancellation efforts have offered significant relief, they underscore the necessity for sustainable, long-term solutions rather than a one-time fix. Additionally, greater attention must be paid to the growing federal deficit, as it could have severe repercussions for the American economy. To genuinely transform higher education, we need to invest in a future that empowers, rather than burdens, the next generation.